Stability, Liquidity, Growth

Listen Now to Will Granleese’s Insight Filled Commentary

- No Historical NAV Volatility

- 6%* Yield

- Quarterly Distributions

No Historical NAV Volatility

Antrim investors have experienced 25 years of a safe and steady NAV. When adding Antrim to a portfolio the expected volatility drops immediately. Advisors, PMs, and clients love the security a stable NAV provides… especially in a rising interest rate environment.

All Antrim mortgages are set up for a 1-year term. After 1 year, the interest rate is reset to the current market rate and the borrower can renew. That means the market value of the mortgage portfolio is always priced at Par. Furthermore, Antrim must pay out 100% of net income to investors every year. It is the combination of no retained earnings and no change in value of the mortgage portfolio that provides no NAV volatility. NAV is struck once a year on June 30th, the financial year end.

A Superior Yield

Investors love the yield Antrim brings to a portfolio. Especially in inflationary and rising rate environments. During the economic crisis of 2009 Antrim investors earned over 10%.

Antrim charges higher rates than the Bank. We lend to borrowers who do not meet the Banks strict debt servicing ratios. Our borrowers have excellent credit scores but due to self-employment and income splitting techniques they might not claim as much income as their salaried employees. This might have the positive effect of them paying lower income taxes, but they do not show enough income to meet the strict debt servicing ratios at the Bank. As a matter of fact, we have several major Banks in Canada that refer these clients to Antrim. We wholesale the loans until they can qualify back to prime rates.

Borrowers take a mortgage from Antrim for 1 year while they try and fix their income. If they need to be renewed, we do so at current rates for another 1-year term. The average Antrim borrower stays with us for about 3 years.

Real Security

Target Asset Allocation

2100 Mortgages in the Pool.

Over 50 years in the mortgage market has taught us one important lesson; do not lose money. To this end Antrim’s target asset allocation is 75% in first mortgages and 25% in second mortgages. Investors are allocated over 2100 individual mortgages making the pool incredibly diversified. We lend in major centers of BC, Alberta, and Ontario.

The weighted average loan-to-value of Antrim’s portfolio is about 59%. That means our average borrower puts down over 40% down payment. Why would the Bank not lend to someone with a 40% down payment? Well, if you cannot prove it to the Bank, you can make the payment, they simply cannot do the loan. For many self-employed individuals, high net worth real estate investors and those new to Canada Antrim is the short-term lender that can help. It is due to this real estate security that over the past 25 years Antrim has never had a negative return and averaged over 8%.

Steady Income

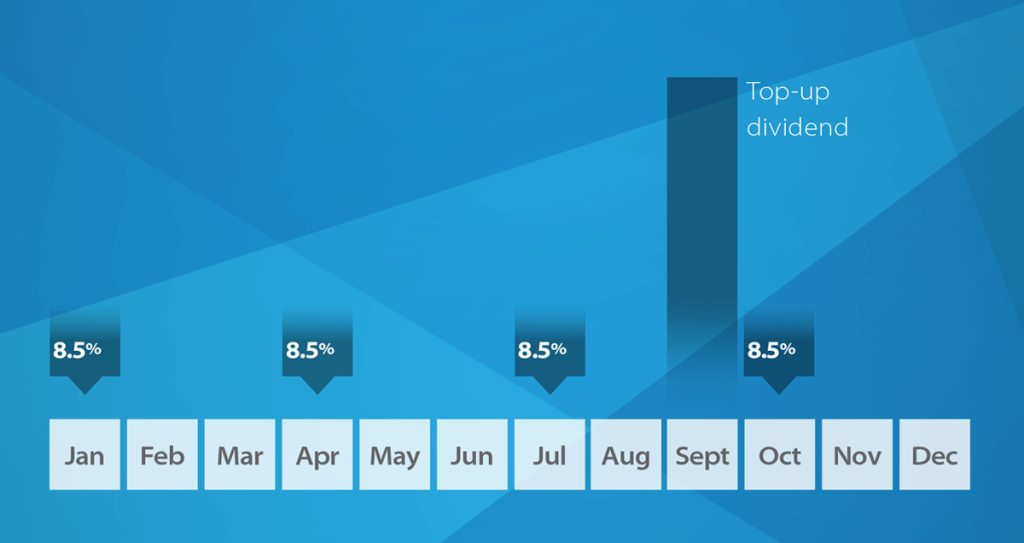

Investors can expect to receive 4 quarterly payments plus one annual top-up. 100% of the next income the Fund earns is paid to investors each year. Antrim has never had a quarter it has not paid a dividend.

Fund Facts

Fund Performance Series (Percent Return)

1 Year

9.08%

3 Years

7.69%

5 Years

7.07%

10 Years

6.96%

Since Inception

6.98%

Antrim Balanced Mortgage Fund

Class Management Fee

Class A, Series A 1%

An Investment That Makes Sense

Antrim does not create yield via complex options strategies that are hard to understand. Most of our investors have a mortgage. Many of our investors have been self employed and had difficulty with a Bank lender. Investors understand our business model.